Federal student loan borrowers can now apply for the SAVE repayment plan—see if you qualify for $0 monthly payments

The Department of Education on Monday released a beta form application for the new Saving on a Valuable Education repayment plan for federal student loan borrowers. The new income-driven repayment plan replaces the Revised Pay as You Earn plan and aims to give borrowers the most affordable monthly payment.

Like REPAYE, the SAVE plan caps monthly payments at a percentage of your discretionary income, currently 10%. Beginning next summer, payments under the SAVE plan will be 5% of your discretionary income, which is the amount of money you earn above 225% of the federal poverty line, about $32,800 a year for individuals in 2023.

Watch NBC6 free wherever you are

>

Borrowers with adjusted gross income at or below that threshold will qualify for $0 monthly payments. That means individuals earning roughly $15 an hour or less will qualify for no monthly payment. Families of four earning $67,500 or less will also owe $0 a month on their loans.

If you have federal direct unsubsidized or subsidized, consolidated, or grad PLUS loans you can apply to enroll in the SAVE plan now on the Federal Student Aid website. Your application will be processed by the time payments resume in October, ED says. If you were already enrolled in the REPAYE plan, you will automatically be transferred into the SAVE plan.

Get local news you need to know to start your day with NBC 6's News Headlines newsletter.

>

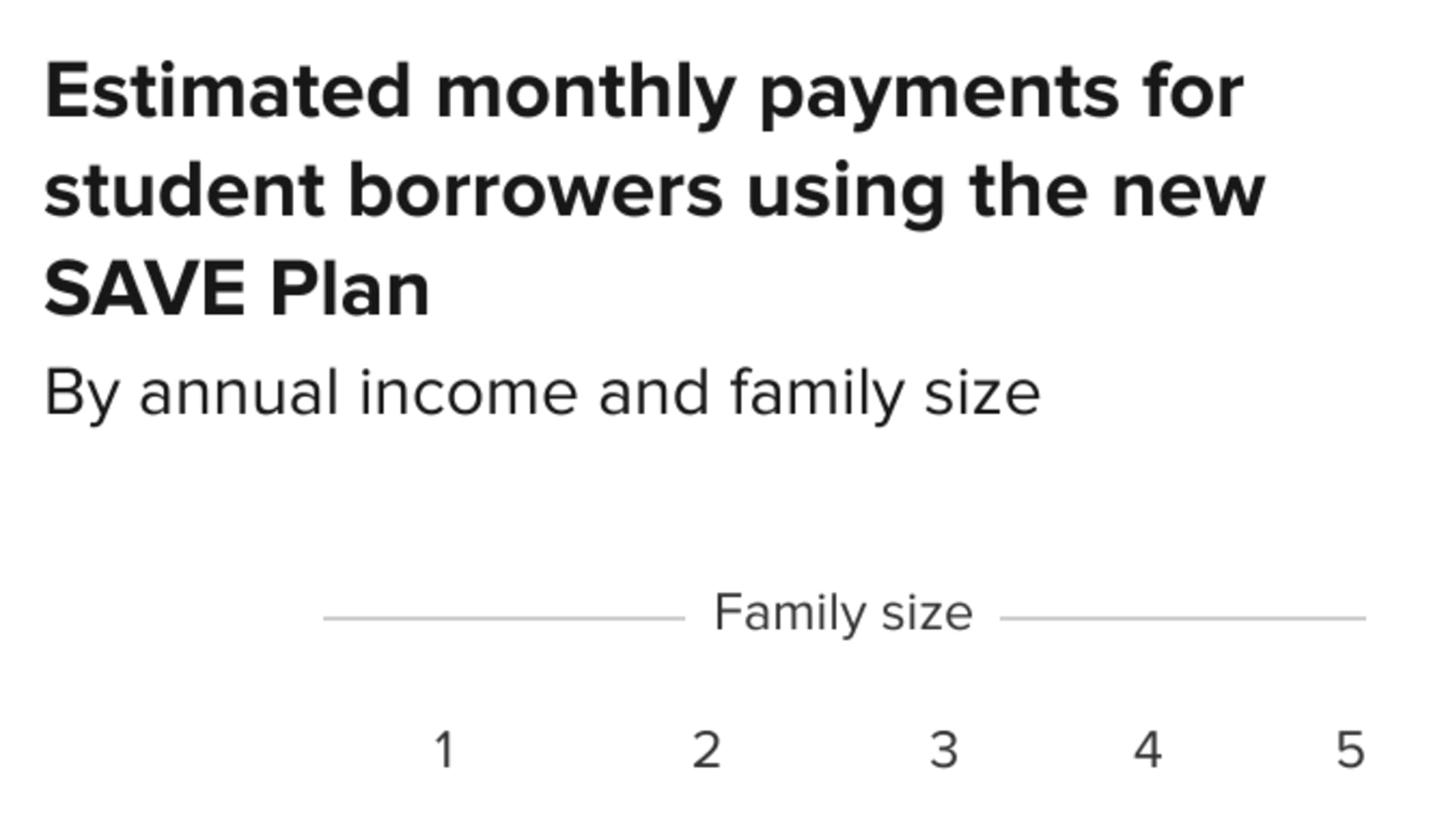

If you earn $60,000 or less, see the chart below for your estimated monthly payment based on your income and family size.

What does a $0 monthly payment mean?

Money Report

It sounds too good to be true, but you really do not need to make a payment if you qualify for a $0 minimum payment on the SAVE plan. That may be a huge relief for low-income borrowers, especially those who have gotten used to making no payments during the pandemic forbearance.

And even if you have a $0 monthly payment, you will still be making progress on your loans because those $0 "payments" count toward the number of payments necessary to be eligible for loan forgiveness through both IDR and Public Service Loan Forgiveness.

Borrowers on all IDR plans are eligible to have their remaining balances forgiven after 20 or 25 years of payments. Those who work in public service as government employees, nonprofit workers, teachers and more can qualify for PSLF after 10 years or 120 monthly payments.

Currently, you need to recertify your income every year that you are on an IDR. But with the rollout of the SAVE application on the Federal Student Aid website, you're able to consent to allow your tax information to automatically recertify your enrollment.

With the SAVE plan, even borrowers who don't qualify for a $0 monthly payment can still save at least $1,000 a year compared with other IDR plans, ED says. Plus, you won't owe excess interest charges on your loans if you meet your monthly payment.

Say your monthly payment is $30 and your loans accrued $50 in interest in a month. You won't be charged that additional $20, according to the FSA website.

DON'T MISS: Want to be smarter and more successful with your money, work & life? Sign up for our new newsletter!

Take your business to the next level: Register for CNBC's free Small Business Playbook virtual event on August 2 at 1 p.m. ET to learn from premier experts and entrepreneurs how you can beat inflation, hire top talent and get access to capital.